Eurofins - Shadowfall aftermath

Pt 9 of the deep dive into Eurofins. Covid interves. Eurofins raise tons of cash and the share price explodes higher.

TL, DR

Nothing refutes a short-sellers accusation of liquidity problems more than running to investors asking them for cash. Eurofins share price explodes on the back of its share issue and positioning as a global covid tester. Does this mean the short-sellers were wrong?

IMPORTANT

Can’t stress this enough, I have no clue whether Eurofins shares will go up, down, sideways or round in circles in the future. I only have interest in the stock price in so far as it’s potential impact on the ability of the criminal justice system in England and Wales to function. Do not, DO NOT, take this as investment advice.

2020

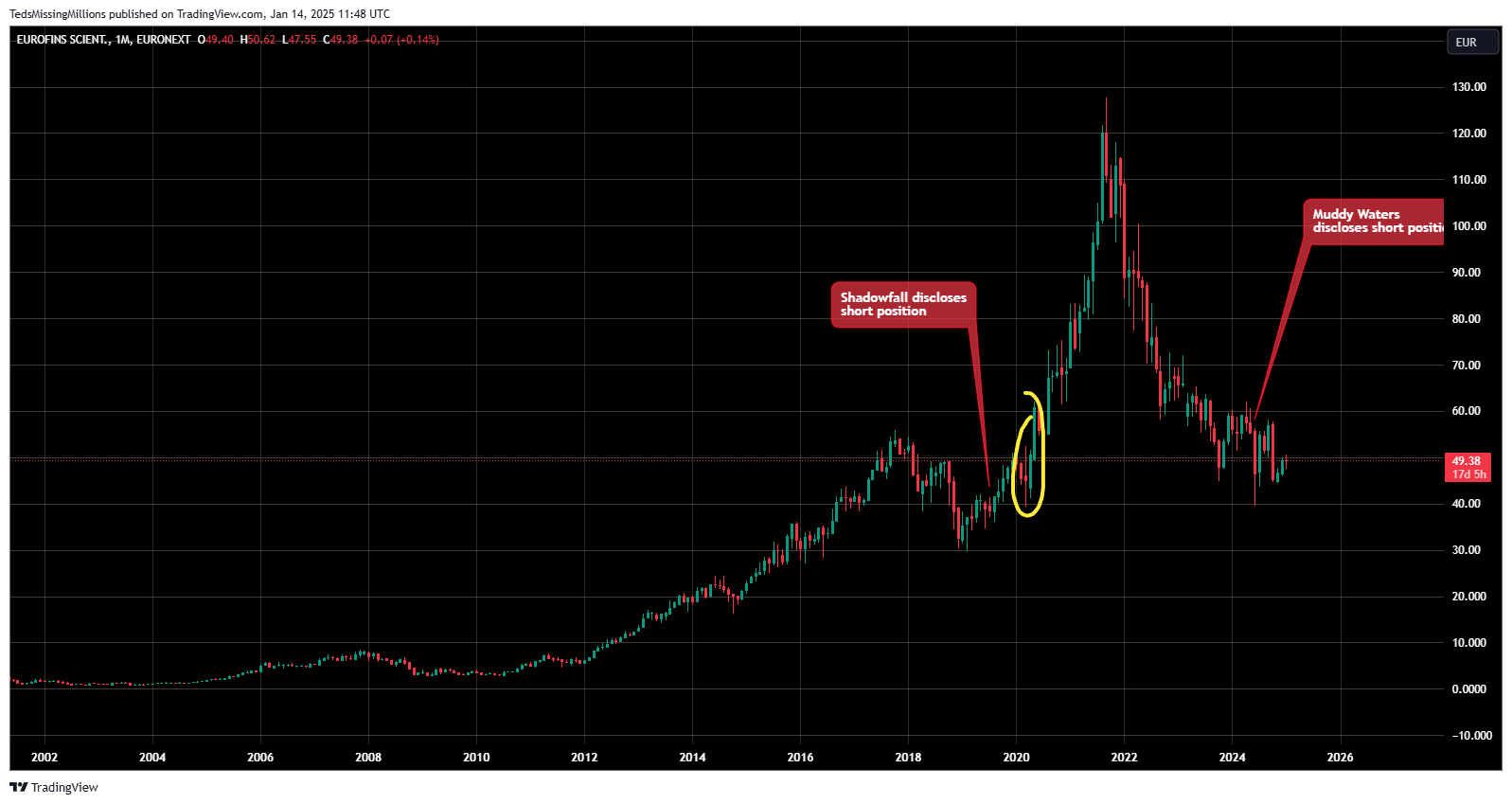

Eurofins having dismissed Shadowfall’s allegations without comprehensively engaging with the 21 specific questions that Shadowfall posed in their dossier, were no doubt pleased to see their share price recover. They must have thought that they had seen off the short sellers with a strong dismissive rebuttal.

The issue for short sellers as shown so clearly in the case of Wirecard, is that they have to be nimble. They know that in market terms they will likely be early, that’s the point of them. It’s easy to make the mistake to think that when an activist short seller publishes their evidence that it represents the precise moment when they have taken a short position, when the reality is that they have probably been building positions for a while, moving in and out of the market as they go. They also hedge their positions in the event the market goes against them. They don’t want to lose money so they may exit their positions if they believe market sentiment is too strong to hold onto their short positions, seeking to rebuild them later at a price of their choosing. Prediciting when bubbles burst is notoriously problemmatic, but short sellers are very good at taking small profits or even losses along the way even when the market goes against them. They only have to be right once to get a big, big pay off. If they believe the core fundamentals which brought them to trade Eurofins short remain in play, there is little reason to change their view. This is likely the reason why Shadowfall has remained “core” short Eurofins since 2019 even though the market clearly had an explosive move to the upside during Covid.

Certainly the market bought into the narrative of Eurofins rebuttal of Shadowfall at least until the pandemic hit in 2020. What we’ll never know is what the market’s true sentiment was concerning Eurofins in the aftermath of Shadowfall’s allegations, the market hadn’t broken through the highs of 2017 and if anything had started to look like it may have been on the turn to the downside.

The global stock market already had become nervous around December 2019 as the pandemic unfolded. The global lockdown in March 2020 and the action of Central Banks left investors wondering what on earth they could do with all this cheap money that they now had access to. Everyone in March 2020 knew the world needed two things and two things only, tests (as a gateway to mobility and work) and vaccines. If you were to get in, best to get in early right?

For Eurofins they must have been thinking that all their ships had come in at once. Here was a massive opportunity to bury any sneaking suspicion (right or wrong) that they really had run out of cash by raising money for covid expansion.

May 2020

Eurofins announces the issuance of c. 900,000 new shares to support its rapid build-up of COVID-19 testing capacities. They raise €535 million a phenomenal amount of cash.

Previously they had raised €299 million 3 years earlier in October 2017, which coincidentally represented close to the height of the market price at €54.3 per share, now they were selling more shares again at similar price of €53.5. In October 2017 the cash was needed to “…enable the Company to maintain a sound capital structure further to the acceleration of its M&A program year-to-date”, whatever that means.

In whatever way they burned through €299 million in 3 years, there didn’t appear to be enough in the piggy banks to fund whatever they had in mind for 2020 and beyond, but to be fair to Eurofins, the pandemic changed everything and they were adept in taking advantage.

Eurofins stated that the €535 million from the issuance of new shares would be used to support the rapid build-up of COVID-19 testing capacities, as well as for other purposes, including:

To further strengthen its current capital structure to be an even stronger company when the COVID-19 crisis will end.

To have more strategic flexibility to seize potential investment opportunities then, with an objective to generate long term shareholder value and create a higher EPS than the dilution impact of the new issuance.

Were Shadowfall right that Eurofins had liquidity problems? If you have no liquidity problems going into a Covid boom, why do you think you need to strengthen when the boom ends? Were they already planning to use the funds raised to buy back shares they had just sold?

May 2020-November 2021

Boom! Free money and huge demand for Covid testing on the back of a huge fund raising event saw the shares explode to nearly €130. But a bubble has to burst eventually and it did in November 2021 when the Federal Reserve indicated it would likely raise interest rates in 2022 to combat rampant inflation. The end of cheap money in otherwords. All the other central banks would follow. Time for speculators to take profits and think about parking them elsewhere.

May 2020-Present

But how far would the share price fall, where did the market think the true value of Eurofins actually lay? When things are going well, no-one gives a hoot, when things are going south, all the real stuff matters. Who are you now post pandemic? How much are you worth? Where and how are you going to grow? Have you grown too far to fast? Have you got the right people in place for the next challenge, etc etc? Can we trust you?

The answer is, the market does not know. But it’s been a huge dump on the share price. From the 2019 low to the 2021 high, Eurofins has lost nearly 80% of those gains in just over 3 years. Dutch tulips much? As of early January 2025 the price is trading at €49, €4 short of the price all those investors bought those shares in 2020 and in 2017.

But, what we do know is in July 2024 another short seller has entered the fight and made some very serious allegations against Eurofins. They are Muddy Waters and their allegations are the subject of a future post.

If Oscar Wilde was a stockbroker he would probably remark that to attract one short-seller may be regarded as unfortunate; to attract two looks like carelessness.

Eurofins, under the current management and ownership are in a massive dogfight and they know it. If the price dips below €40 who knows really where the low might be and in that event, Eurofins may likely become the target of activist hedge funds which could threaten the ownership of the parent company and with it, the future of its subsidiaries including Eurofins Forensic Services Limited here in the UK.

Sometimes these issues take a long time to play out, in other cases a catalyst, like a global stock market shock, or some fundamental economic change like Central Bank interventions or company-specific event (like a huge drop in earnings, a key departure of senior management or catstrophic news event) could trigger a futher run on the stock.

Eurofins latest financial earnings are released on Jan 30 2025. Next up, Eurofins is accused of profiteering during Covid and Shadowfall weighs in (again).